Bank Funding Risk, Reference Rates, and Credit Supply

Abstract

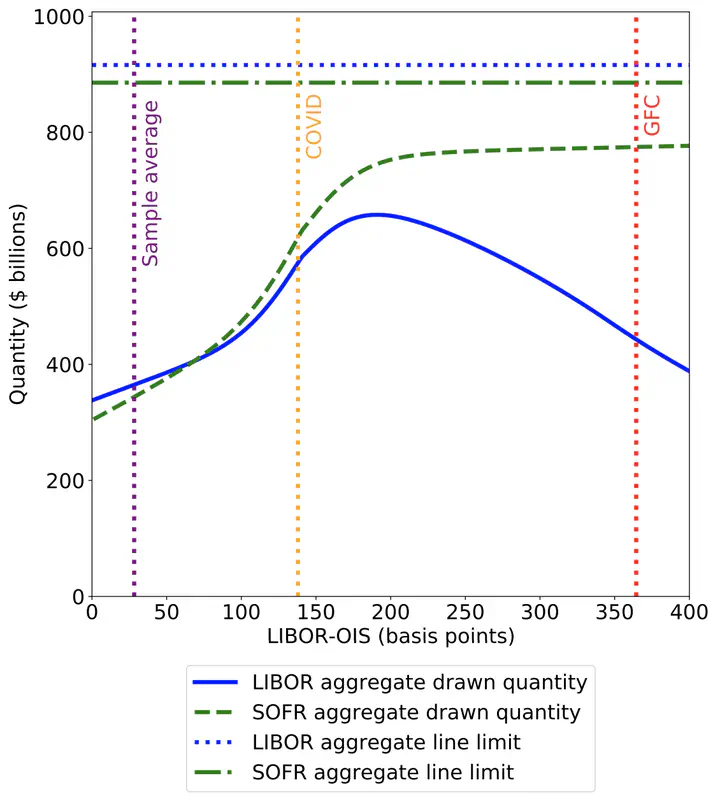

Corporate credit lines are drawn more heavily when funding markets are more stressed. This covariance elevates expected bank funding costs. We show that credit supply is dampened by the associated debt-overhang cost to bank shareholders. Until 2022, this impact was reduced by linking the interest paid on lines to credit-sensitive reference rates such as LIBOR. We show that transition to risk-free reference rates may exacerbate this friction. The adverse impact on credit supply is offset if drawdowns are expected to be left on deposit at the same bank, which happened at some of the largest banks during the COVID recession.

Type

Publication

The Journal of Finance

Yilin (David) Yang

Assistant Professor in Finance

Assistant Professor of Finance at the University of Minnesota Twin Cities