2

Transition from credit-sensitive benchmarks like LIBOR to risk-free rates like SOFR can quietly tighten credit supply.

Abstract

Corporate credit lines are drawn more heavily when funding markets are more stressed. This covariance elevates expected bank funding costs. We show that credit supply is dampened by the associated debt-overhang cost to bank shareholders. Until 2022, this impact was reduced by linking the interest paid on lines to credit-sensitive reference rates such as LIBOR. We show that transition to risk-free reference rates may exacerbate this friction. The adverse impact on credit supply is offset if drawdowns are expected to be left on deposit at the same bank, which happened at some of the largest banks during the COVID recession.

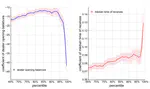

Quantitative Tightening increases the risk of a dollar funding squeeze. Delayed intraday payments to the largest dealer banks may act as an early-warning signal.

Abstract

We show that the likelihood of a liquidity crunch in wholesale US dollar funding markets is highly dependent on levels of reserve balances at the financial institutions that are the most active intermediaries of these markets. Heightened risk of an imminent liquidity crunch is signaled by significant delays in intra-day payments to these large financial institutions over the prior two weeks. Our study contributes to the broader dialogue surrounding the Federal Reserve’s ongoing quantitative tightening (QT).