What Quantity of Reserves Is Sufficient?

Abstract

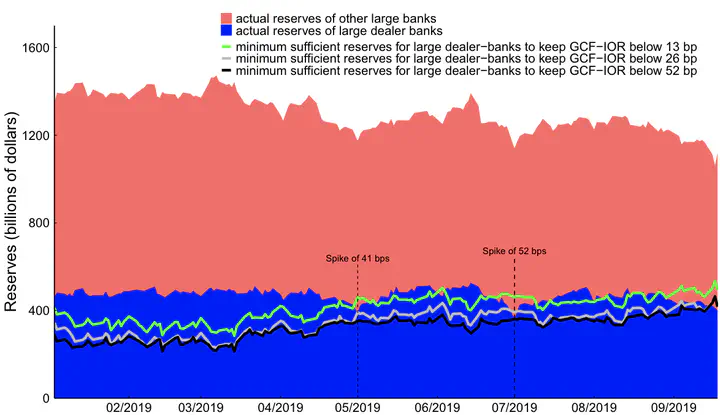

What quantity of reserves is sufficient to support effective monetary policy implementation and an efficient interbank payment system? To answer this question, I construct a model that links interbank intraday payment timing to monetary policy implementation. I show that a low reserve supply causes banks to delay payments to each other and strategically hoard reserves, which in turn disincentivizes banks from providing liquidity to short-term funding markets, driving up the spreads between overnight risk-free market rates and the central bank deposit rate and, impeding monetary policy implementation. As reserve balances get sufficiently low, even small reductions in reserves can have large impacts on these spreads, mirroring the repo-spike event observed in September 2019. The model also provides a counterfactual analysis of the sufficient reserve level that could have prevented the September 2019 repo spike, offering insights into the current discussions about the appropriate size of the Federal Reserve’s balance sheet.

WFA 2022 Brattle Group Ph.D. Candidate Awards For Outstanding Research

The BlackRock Applied Research Award 2021 (runner-up)

Yilin (David) Yang

Assistant Professor in Finance

Assistant Professor of Finance at the University of Minnesota Twin Cities