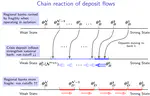

Strategic Complementarity

A slightly more stable national bank drains deposits from regional neighbors during crises, endogenously strengthening the national bank and weakening the regional ones. Implication: Macroprudential policies calibrated on isolated single-bank models tend to over-fortify national institutions.

Abstract

This paper identifies a novel bank-run externality: when depositors can shift funds across risky banks in a crisis, a large national bank perceived as safer may disproportionately raise the likelihood of runs among smaller regional banks. A minor shock can prompt a cascading chain reaction of deposit withdrawals among many regional banks, generating systemic vulnerabilities beyond traditional interbank-contagion channels. We extend global game models by allowing realistic deposit mobility across multiple risky banks, alongside the conventional risk-free option. Our framework captures the interaction between strategic complementarity in run/stay decisions among multiple substitutes—a dynamic that remains underexplored in the literature.

- Generalized global-games bank run models with multiple run options

Low reserve supply causes banks to strategically delay payments and hoard liquidity, impeding monetary policy implementation. A game-theoretic model calibrated using 2019 data offers a quantitative framework to determine the minimum sufficient size of the Federal Reserve’s balance sheet.

Abstract

What quantity of reserves is sufficient to support effective monetary policy implementation and an efficient interbank payment system? To answer this question, I construct a model that links interbank intraday payment timing to monetary policy implementation. I show that a low reserve supply causes banks to delay payments to each other and strategically hoard reserves, which in turn disincentivizes banks from providing liquidity to short-term funding markets, driving up the spreads between overnight risk-free market rates and the central bank deposit rate and, impeding monetary policy implementation. As reserve balances get sufficiently low, even small reductions in reserves can have large impacts on these spreads, mirroring the repo-spike event observed in September 2019. The model also provides a counterfactual analysis of the sufficient reserve level that could have prevented the September 2019 repo spike, offering insights into the current discussions about the appropriate size of the Federal Reserve’s balance sheet.

- Revise & Resubmit, JFE

- WFA 2022 Brattle Group Ph.D. Candidate Awards For Outstanding Research

- The BlackRock Applied Research Award 2021 (runner-up)